Ensemble learning¶

- If different models make different mistakes, can we simply average the predictions?

- Voting Classifier: gives every model a vote on the class label

- Hard vote: majority class wins (class order breaks ties)

- Soft vote: sum class probabilities $p_{m,c}$ over $M$ models: $\underset{c}{\operatorname{argmax}} \sum_{m=1}^{M} w_c p_{m,c}$

- Classes can get different weights $w_c$ (default: $w_c=1$)

interactive(children=(Dropdown(description='model1', options=(LogisticRegression(C=100), DecisionTreeClassifie…

- Why does this work?

- Different models may be good at different 'parts' of data (even if they underfit)

- Individual mistakes can be 'averaged out' (especially if models overfit)

- Which models should be combined?

- Bias-variance analysis teaches us that we have two options:

- If model underfits (high bias, low variance): combine with other low-variance models

- Need to be different: 'experts' on different parts of the data

- Bias reduction. Can be done with Boosting

- If model overfits (low bias, high variance): combine with other low-bias models

- Need to be different: individual mistakes must be different

- Variance reduction. Can be done with Bagging

- If model underfits (high bias, low variance): combine with other low-variance models

- Models must be uncorrelated but good enough (otherwise the ensemble is worse)

- We can also learn how to combine the predictions of different models: Stacking

Decision trees (recap)¶

- Representation: Tree that splits data points into leaves based on tests

- Evaluation (loss): Heuristic for purity of leaves (Gini index, entropy,...)

- Optimization: Recursive, heuristic greedy search (Hunt's algorithm)

- Consider all splits (thresholds) between adjacent data points, for every feature

- Choose the one that yields the purest leafs, repeat

interactive(children=(IntSlider(value=3, description='depth', max=5, min=1), Output()), _dom_classes=('widget-…

Evaluation (loss function for classification)¶

- Every leaf predicts a class probability $\hat{p}_c$ = the relative frequency of class $c$

- Leaf impurity measures (splitting criteria) for $L$ leafs, leaf $l$ has data $X_l$:

- Gini-Index: $Gini(X_{l}) = \sum_{c\neq c'} \hat{p}_c \hat{p}_{c'}$

- Entropy (more expensive): $E(X_{l}) = -\sum_{c\neq c'} \hat{p}_c \log_{2}\hat{p}_c$

- Best split maximizes information gain (idem for Gini index) $$ Gain(X,X_i) = E(X) - \sum_{l=1}^L \frac{|X_{i=l}|}{|X_{i}|} E(X_{i=l}) $$

Regression trees¶

- Every leaf predicts the mean target value $\mu$ of all points in that leaf

- Choose the split that minimizes squared error of the leaves: $\sum_{x_{i} \in L} (y_i - \mu)^2$

- Yields non-smooth step-wise predictions, cannot extrapolate

Impurity/Entropy-based feature importance¶

- We can measure the importance of features (to the model) based on

- Which features we split on

- How high up in the tree we split on them (first splits ar emore important)

Under- and overfitting¶

- We can easily control the (maximum) depth of the trees as a hyperparameter

- Bias-variance analysis:

- Shallow trees have high bias but very low variance (underfitting)

- Deep trees have high variance but low bias (overfitting)

- Because we can easily control their complexity, they are ideal for ensembling

- Deep trees: keep low bias, reduce variance with Bagging

- Shallow trees: keep low variance, reduce bias with Boosting

Bagging (Bootstrap Aggregating)¶

- Obtain different models by training the same model on different training samples

- Reduce overfitting by averaging out individual predictions (variance reduction)

- In practice: take $I$ bootstrap samples of your data, train a model on each bootstrap

- Higher $I$: more models, more smoothing (but slower training and prediction)

- Base models should be unstable: different training samples yield different models

- E.g. very deep decision trees, or even randomized decision trees

- Deep Neural Networks can also benefit from bagging (deep ensembles)

- Prediction by averaging predictions of base models

- Soft voting for classification (possibly weighted)

- Mean value for regression

- Can produce uncertainty estimates as well

- By combining class probabilities of individual models (or variances for regression)

Random Forests¶

- Uses randomized trees to make models even less correlated (more unstable)

- At every split, only consider

max_featuresfeatures, randomly selected

- At every split, only consider

- Extremely randomized trees: considers 1 random threshold for random set of features (faster)

interactive(children=(Dropdown(description='model', options=(RandomForestClassifier(n_estimators=5, n_jobs=-1,…

Effect on bias and variance¶

- Increasing the number of models (trees) decreases variance (less overfitting)

- Bias is mostly unaffected, but will increase if the forest becomes too large (oversmoothing)

In practice¶

Different implementations can be used. E.g. in scikit-learn:

BaggingClassifier: Choose your own base model and sampling procedureRandomForestClassifier: Default implementation, many optionsExtraTreesClassifier: Uses extremely randomized trees

Most important parameters:

n_estimators(>100, higher is better, but diminishing returns)- Will start to underfit (bias error component increases slightly)

max_features- Defaults: $sqrt(p)$ for classification, $log2(p)$ for regression

- Set smaller to reduce space/time requirements

- parameters of trees, e.g.

max_depth,min_samples_split,...- Prepruning useful to reduce model size, but don't overdo it

Easy to parallelize (set

n_jobsto -1)- Fix

random_state(bootstrap samples) for reproducibility

Out-of-bag error¶

- RandomForests don't need cross-validation: you can use the out-of-bag (OOB) error

- For each tree grown, about 33% of samples are out-of-bag (OOB)

- Remember which are OOB samples for every model, do voting over these

- OOB error estimates are great to speed up model selection

- As good as CV estimates, althought slightly pessimistic

- In scikit-learn:

oob_error = 1 - clf.oob_score_

Feature importance¶

- RandomForests provide more reliable feature importances, based on many alternative hypotheses (trees)

Other tips¶

- Model calibration

- RandomForests are poorly calibrated.

- Calibrate afterwards (e.g. isotonic regression) if you aim to use probabilities

- Warm starting

- Given an ensemble trained for $I$ iterations, you can simply add more models later

- You warm start from the existing model instead of re-starting from scratch

- Can be useful to train models on new, closely related data

- Not ideal if the data batches change over time (concept drift)

- Boosting is more robust against this (see later)

Strength and weaknesses¶

- RandomForest are among most widely used algorithms:

- Don't require a lot of tuning

- Typically very accurate

- Handles heterogeneous features well (trees)

- Implictly selects most relevant features

- Downsides:

- less interpretable, slower to train (but parallellizable)

- don't work well on high dimensional sparse data (e.g. text)

Adaptive Boosting (AdaBoost)¶

- Obtain different models by reweighting the training data every iteration

- Reduce underfitting by focusing on the 'hard' training examples

- Increase weights of instances misclassified by the ensemble, and vice versa

- Base models should be simple so that different instance weights lead to different models

- Underfitting models: decision stumps (or very shallow trees)

- Each is an 'expert' on some parts of the data

- Additive model: Predictions at iteration $I$ are sum of base model predictions

- In Adaboost, also the models each get a unique weight $w_i$ $$f_I(\mathbf{x}) = \sum_{i=1}^I w_i g_i(\mathbf{x})$$

- Adaboost minimizes exponential loss. For instance-weighted error $\varepsilon$: $$\mathcal{L}_{Exp} = \sum_{n=1}^N e^{\varepsilon(f_I(\mathbf{x}))}$$

- By deriving $\frac{\partial \mathcal{L}}{\partial w_i}$ you can find that optimal $w_{i} = \frac{1}{2}\log(\frac{1-\varepsilon}{\varepsilon})$

AdaBoost algorithm¶

- Initialize sample weights: $s_{n,0} = \frac{1}{N}$

- Build a model (e.g. decision stumps) using these sample weights

- Give the model a weight $w_i$ related to its weighted error rate $\varepsilon$

$$w_{i} = \lambda\log(\frac{1-\varepsilon}{\varepsilon})$$

- Good trees get more weight than bad trees

- Logit function maps error $\varepsilon$ from [0,1] to weight in [-Inf,Inf] (use small minimum error)

- Learning rate $\lambda$ (shrinkage) decreases impact of individual classifiers

- Small updates are often better but requires more iterations

- Update the sample weights

- Increase weight of incorrectly predicted samples: $s_{n,i+1} = s_{n,i}e^{w_i}$

- Decrease weight of correctly predicted samples: $s_{n,i+1} = s_{n,i}e^{-w_i}$

- Normalize weights to add up to 1

- Repeat for $I$ iterations

AdaBoost variants¶

- Discrete Adaboost: error rate $\varepsilon$ is simply the error rate (1-Accuracy)

- Real Adaboost: $\varepsilon$ is based on predicted class probabilities $\hat{p}_c$ (better)

- AdaBoost for regression: $\varepsilon$ is either linear ($|y_i-\hat{y}_i|$), squared ($(y_i-\hat{y}_i)^2$), or exponential loss

- GentleBoost: adds a bound on model weights $w_i$

- LogitBoost: Minimizes logistic loss instead of exponential loss $$\mathcal{L}_{Logistic} = \sum_{n=1}^N log(1+e^{\varepsilon(f_I(\mathbf{x}))})$$

Adaboost in action¶

- Size of the samples represents sample weight

- Background shows the latest tree's predictions

interactive(children=(IntSlider(value=30, description='iteration', max=60), Output()), _dom_classes=('widget-i…

Examples¶

Bias-Variance analysis¶

- AdaBoost reduces bias (and a little variance)

- Boosting is a bias reduction technique

- Boosting too much will eventually increase variance

Gradient Boosting¶

- Ensemble of models, each fixing the remaining mistakes of the previous ones

- Each iteration, the task is to predict the residual error of the ensemble

- Additive model: Predictions at iteration $I$ are sum of base model predictions

- Learning rate (or shrinkage ) $\eta$: small updates work better (reduces variance) $$f_I(\mathbf{x}) = g_0(\mathbf{x}) + \sum_{i=1}^I \eta \cdot g_i(\mathbf{x}) = f_{I-1}(\mathbf{x}) + \eta \cdot g_I(\mathbf{x})$$

- The pseudo-residuals $r_i$ are computed according to differentiable loss function

- E.g. least squares loss for regression and log loss for classification

- Gradient descent: predictions get updated step by step until convergence $$g_i(\mathbf{x}) \approx r_{i} = - \frac{\partial \mathcal{L}(y_i,f_{i-1}(x_i))}{\partial f_{i-1}(x_i)}$$

- Base models $g_i$ should be low variance, but flexible enough to predict residuals accurately

- E.g. decision trees of depth 2-5

Gradient Boosting Trees (Regression)¶

- Base models are regression trees, loss function is square loss: $\mathcal{L} = \frac{1}{2}(y_i - \hat{y}_i)^2$

- The pseudo-residuals are simply the prediction errors for every sample: $$r_i = -\frac{\partial \mathcal{L}}{\partial \hat{y}} = -2 * \frac{1}{2}(y_i - \hat{y}_i) * (-1) = y_i - \hat{y}_i$$

- Initial model $g_0$ simply predicts the mean of $y$

For iteration $m=1..M$:

- For all samples i=1..n, compute pseudo-residuals $r_i = y_i - \hat{y}_i$

- Fit a new regression tree model $g_m(\mathbf{x})$ to $r_{i}$

- In $g_m(\mathbf{x})$, each leaf predicts the mean of all its values

- Update ensemble predictions $\hat{y} = g_0(\mathbf{x}) + \sum_{m=1}^M \eta \cdot g_m(\mathbf{x})$

Early stopping (optional): stop when performance on validation set does not improve for $nr$ iterations

Gradient Boosting Regression in action¶

- Residuals quickly drop to (near) zero

interactive(children=(IntSlider(value=30, description='step', max=60), Output()), _dom_classes=('widget-intera…

GradientBoosting Algorithm (Classification)¶

- Base models are regression trees, predict probability of positive class $p$

- For multi-class problems, train one tree per class

- Use (binary) log loss, with true class $y_i \in {0,1}$: $\mathcal{L_{log}} = - \sum_{i=1}^{N} \big[ y_i log(p_i) + (1-y_i) log(1-p_i) \big] $

- The pseudo-residuals are simply the difference between true class and predicted $p$: $$\frac{\partial \mathcal{L}}{\partial \hat{y}} = \frac{\partial \mathcal{L}}{\partial log(p_i)} = y_i - p_i$$

- Initial model $g_0$ predicts $p = log(\frac{\#positives}{\#negatives})$

- For iteration $m=1..M$:

- For all samples i=1..n, compute pseudo-residuals $r_i = y_i - p_i$

- Fit a new regression tree model $g_m(\mathbf{x})$ to $r_{i}$

- In $g_m(\mathbf{x})$, each leaf predicts $\frac{\sum_{i} r_i}{\sum_{i} p_i(1-p_i)}$

- Update ensemble predictions $\hat{y} = g_0(\mathbf{x}) + \sum_{m=1}^M \eta \cdot g_m(\mathbf{x})$

- Early stopping (optional): stop when performance on validation set does not improve for $nr$ iterations

Gradient Boosting Classification in action¶

- Size of the samples represents the residual weights: most quickly drop to (near) zero

interactive(children=(IntSlider(value=30, description='iteration', max=60, min=1), Output()), _dom_classes=('w…

Examples¶

Bias-variance analysis¶

- Gradient Boosting is very effective at reducing bias error

- Boosting too much will eventually increase variance

Feature importance¶

- Gradient Boosting also provide feature importances, based on many trees

- Compared to RandomForests, the trees are smaller, hence more features have zero importance

Gradient Boosting: strengths and weaknesses¶

- Among the most powerful and widely used models

- Work well on heterogeneous features and different scales

- Typically better than random forests, but requires more tuning, longer training

- Does not work well on high-dimensional sparse data

Main hyperparameters:

n_estimators: Higher is better, but will start to overfitlearning_rate: Lower rates mean more trees are needed to get more complex models- Set

n_estimatorsas high as possible, then tunelearning_rate - Or, choose a

learning_rateand use early stopping to avoid overfitting

- Set

max_depth: typically kept low (<5), reduce when overfittingmax_features: can also be tuned, similar to random forestsn_iter_no_change: early stopping: algorithm stops if improvement is less than a certain tolerancetolfor more thann_iter_no_changeiterations.

Extreme Gradient Boosting (XGBoost)¶

- Faster version of gradient boosting: allows more iterations on larger datasets

- Normal regression trees: split to minimize squared loss of leaf predictions

- XGBoost trees only fit residuals: split so that residuals in leaf are more similar

- Don't evaluate every split point, only $q$ quantiles per feature (binning)

- $q$ is hyperparameter (

sketch_eps, default 0.03)

- $q$ is hyperparameter (

- For large datasets, XGBoost uses approximate quantiles

- Can be parallelized (multicore) by chunking the data and combining histograms of data

- For classification, the quantiles are weighted by $p(1-p)$

- Gradient descent sped up by using the second derivative of the loss function

- Strong regularization by pre-pruning the trees

- Column and row are randomly subsampled when computing splits

- Support for out-of-core computation (data compression in RAM, sharding,...)

XGBoost in practice¶

- Not part of scikit-learn, but

HistGradientBoostingClassifieris similar- binning, multicore,...

- The

xgboostpython package is sklearn-compatible- Install separately,

conda install -c conda-forge xgboost - Allows learning curve plotting and warm-starting

- Install separately,

- Further reading:

LightGBM¶

Another fast boosting technique

- Uses gradient-based sampling

- use all instances with large gradients/residuals (e.g. 10% largest)

- randomly sample instances with small gradients, ignore the rest

- intuition: samples with small gradients are already well-trained.

- requires adapted information gain criterion

- Does smarter encoding of categorical features

CatBoost¶

Another fast boosting technique

- Optimized for categorical variables

- Uses bagged and smoothed version of target encoding

- Uses symmetric trees: same split for all nodes on a given level aka

- Can be much faster

- Allows monotonicity constraints for numeric features

- Model must be be a non-decreasing function of these features

- Lots of tooling (e.g. GPU training)

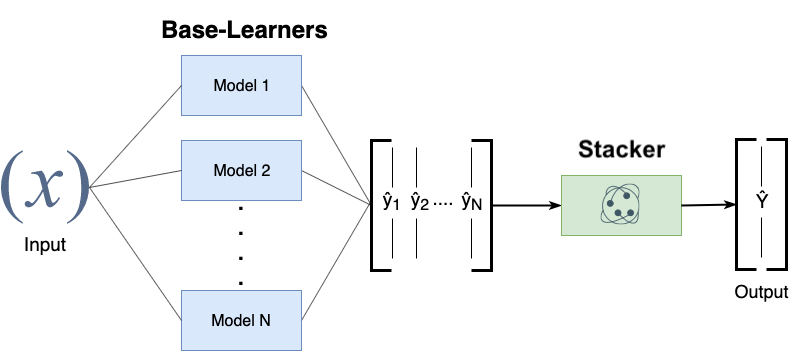

Stacking¶

- Choose $M$ different base-models, generate predictions

- Stacker (meta-model) learns mapping between predictions and correct label

- Can also be repeated: multi-level stacking

- Popular stackers: linear models (fast) and gradient boosting (accurate)

- Cascade stacking: adds base-model predictions as extra features

- Models need to be sufficiently different, be experts at different parts of the data

- Can be very accurate, but also very slow to predict

Other ensembling techniques¶

- Hyper-ensembles: same basic model but with different hyperparameter settings

- Can combine overfitted and underfitted models

- Deep ensembles: ensembles of deep learning models

- Bayes optimal classifier: ensemble of all possible models (largely theoretic)

- Bayesian model averaging: weighted average of probabilistic models, weighted by their posterior probabilities

- Cross-validation selection: does internal cross-validation to select best of $M$ models

- Any combination of different ensembling techniques

Algorithm overview¶

| Name | Representation | Loss function | Optimization | Regularization |

|---|---|---|---|---|

| Classification trees | Decision tree | Entropy / Gini index | Hunt's algorithm | Tree depth,... |

| Regression trees | Decision tree | Square loss | Hunt's algorithm | Tree depth,... |

| RandomForest | Ensemble of randomized trees | Entropy / Gini / Square | (Bagging) | Number/depth of trees,... |

| AdaBoost | Ensemble of stumps | Exponential loss | Greedy search | Number/depth of trees,... |

| GradientBoostingRegression | Ensemble of regression trees | Square loss | Gradient descent | Number/depth of trees,... |

| GradientBoostingClassification | Ensemble of regression trees | Log loss | Gradient descent | Number/depth of trees,... |

| XGBoost, LightGBM, CatBoost | Ensemble of XGBoost trees | Square/log loss | 2nd order gradients | Number/depth of trees,... |

| Stacking | Ensemble of heterogeneous models | / | / | Number of models,... |

Summary¶

- Ensembles of voting classifiers improve performance

- Which models to choose? Consider bias-variance tradeoffs!

- Bagging / RandomForest is a variance-reduction technique

- Build many high-variance (overfitting) models on random data samples

- The more different the models, the better

- Aggregation (soft voting) over many models reduces variance

- Diminishing returns, over-smoothing may increase bias error

- Parallellizes easily, doesn't require much tuning

- Build many high-variance (overfitting) models on random data samples

- Boosting is a bias-reduction technique

- Build low-variance models that correct each other's mistakes

- By reweighting misclassified samples: AdaBoost

- By predicting the residual error: Gradient Boosting

- Additive models: predictions are sum of base-model predictions

- Can drive the error to zero, but risk overfitting

- Doesn't parallelize easily. Slower to train, much faster to predict.

- XGBoost,LightGBM,... are fast and offer some parallellization

- Build low-variance models that correct each other's mistakes

- Stacking: learn how to combine base-model predictions

- Base-models still have to be sufficiently different